Overview

In the modern creator economy, scaling digital campaigns and managing software expenses requires specialized financial tools. Standard credit cards frequently trigger payment bans on ad networks and struggle with high-volume international transactions. Virtual Credit Cards (VCCs) solve these friction points by providing flexible underwriting, deep BIN pools, and seamless cross-border funding rails.

Key Highlights & Top Providers

- Creator-Focused Underwriting: Platforms like Karat Financial bypass traditional credit scores, assessing social media metrics and engagement to offer high credit lines without personal guarantees.

- Ad Campaign Scaling & Security: Providers like PST.NET and Spendge are engineered for media buyers, offering platform-specific cards and fresh BINs to prevent ad account bans on Meta, Google, and TikTok.

- High-Volume Capital Efficiency: Juni and Ramp offer massive daily limits, automated expense tracking, and flat-rate cashback (up to 1.5%) to optimize digital marketing return on investment (ROI).

- Web3 Integration: The rise of decentralized finance has introduced options like the MetaMask Card and Oobit, enabling creators to instantly convert and spend stablecoins ($USDT$/$USDC$) for real-world expenses.

Choosing the Right Infrastructure

Depending on your operational geography and workflows, the optimal payment infrastructure varies:

| Needs / Focus Region | Recommended Platform | Key Advantage |

| Social-Based Credit Lines | Karat Financial | $50,000+ starting limits via social metrics |

| Media Buying Protection | PST.NET / Spendge | Large pools of trusted BINs for ad platforms |

| Indian Digital Market | Karbon Business / Happay | Inward remittance management with low/0% FX markups |

| Crypto/Web3 Liquidity | MetaMask Card / Fasset | Instant token-to-fiat conversion at checkout |

Strategic Takeaway: Relying on a single, physical credit card creates catastrophic vulnerabilities for digital publishers. Funneling your affiliate revenue into automated, programmable virtual credit cards ensures your campaigns remain secure, isolated from risk, and highly scalable.

Table of Contents

Introduction

In our foundational guide to the creator economy, we explored how Virtual Credit Cards (VCCs) and sub-affiliate networks like Cuelinks are eliminating financial friction for digital publishers.

We’ve already covered the mechanics of tokenization, the flaws of legacy cross-border payouts, and the strategic differences between single-use, subscription, and media-buying cards.

Now, it is time to put that strategy into practice.

If you are routing your Cuelinks commission payouts into scaling ad campaigns on Meta, Google, or TikTok, or if you are managing recurring software subscriptions for your agency, you need the right financial infrastructure.

This guide dives straight into the top 10 virtual card providers serving the creator economy and performance marketing sectors in 2026, helping you choose the best platform to deploy your earnings securely and profitably.

Strategic Alignment: Evaluating Virtual Card Providers

Selecting the optimal virtual card provider requires analyzing a matrix of features that directly impact digital marketing workflows.

| Evaluative Criterion | Operational Implication for Creators and Affiliates |

| Multi-BIN Support | Distinct BINs across multiple regions (US, EU, UK, HK) allow media buyers to match ad platform billing environments, maximizing approval rates. |

| Liquidity and Funding Rails | Speed of topping up balances. Platforms supporting fiat (ACH, SEPA) and stablecoins (USDT, USDC) ensure campaigns run 24/7. |

| Cashback and Rewards | Flat-rate or tiered cashback structures (0.5% to 3%) transform ad spend into a revenue-generating asset, boosting overall ROAS. |

| Expense Management | Native integration with accounting software, optical character recognition (OCR) for receipts, and multi-tier team approvals. |

| Foreign Exchange (FX) | The percentage applied outside the base currency. Excessive FX markups can destroy profit margins in cross-border arbitrage. |

Top 10 Virtual Payment Cards for Digital Marketers

1. Karat Financial: The Creator-Native Underwriting Model

Karat Financial has fundamentally redefined the underwriting process for content creators, influencers, and digital agencies.

- Alternative Underwriting: Traditional banks rely on FICO scores, which disadvantages digital creators. Karat evaluates your social media metrics, audience engagement, and real-time cash flow instead.

- High Credit Lines: The Karat Black and Max Cards provide substantial credit lines (often starting at $50,000) without requiring a personal guarantee.

- Creator-Tailored Rewards: Earn 1% to 3% back on spending. Points can be redeemed for statement credits or high-visibility assets like Times Square billboards.

- All-in-One Dashboard: Features include high-yield business checking (up to 2.75% APY), automated invoicing, and AI-assisted bookkeeping.

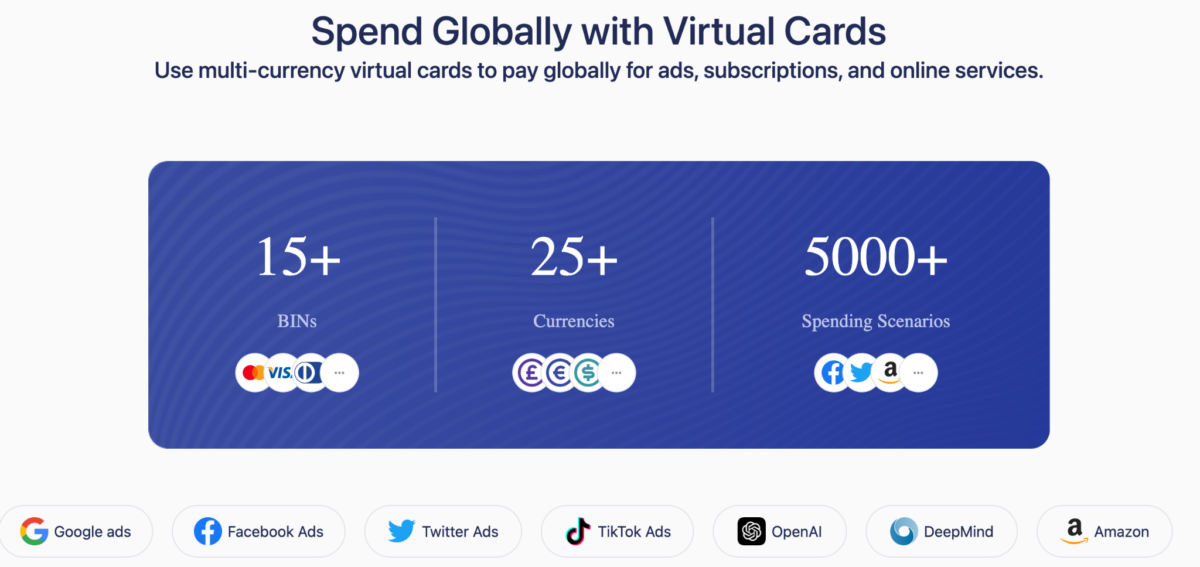

2. PST.NET: The Affiliate and Media Buying Powerhouse

PST.NET is precision-engineered to solve the most prominent pain point in digital marketing: payment method bans on platforms like Meta, Google, and TikTok.

- Deep BIN Pools: Access to over 22 premium BINs sourced from major US and European acquiring banks ensures fresh, high-trust credentials.

- Platform-Specific Cards: Dedicated cards optimized for Facebook Ads (17 BINs), Google Ads (12 BINs), and TikTok Ads (3 BINs).

- Crypto Liquidity: Supports seamless cryptocurrency funding via USDT (TRC20) or Bitcoin, bypassing traditional wire transfer delays.

- Elite Tiers: The “PST Private” program provides high-volume users with up to 100 free virtual cards and an aggressive 3% cashback on advertising spend.

3. Spendge: The Global Traffic Arbitrage Engine

Spendge operates as a highly scalable virtual card issuing technology built explicitly for traffic arbitrage and performance marketing.

- Geographic Diversity: Provides 24 distinct BINs (GBP, USD, EUR) across the UK, Estonia, Ireland, US, and Hong Kong to match geographic ad targeting.

- Ads Cards: Optimized for bulk issuance, trusted BINs, and per-card 3D-Secure controls.

- Unified Account Balance: Top up a central pool with USDT. Funds are deducted centrally, eliminating the need to manually pre-load individual cards.

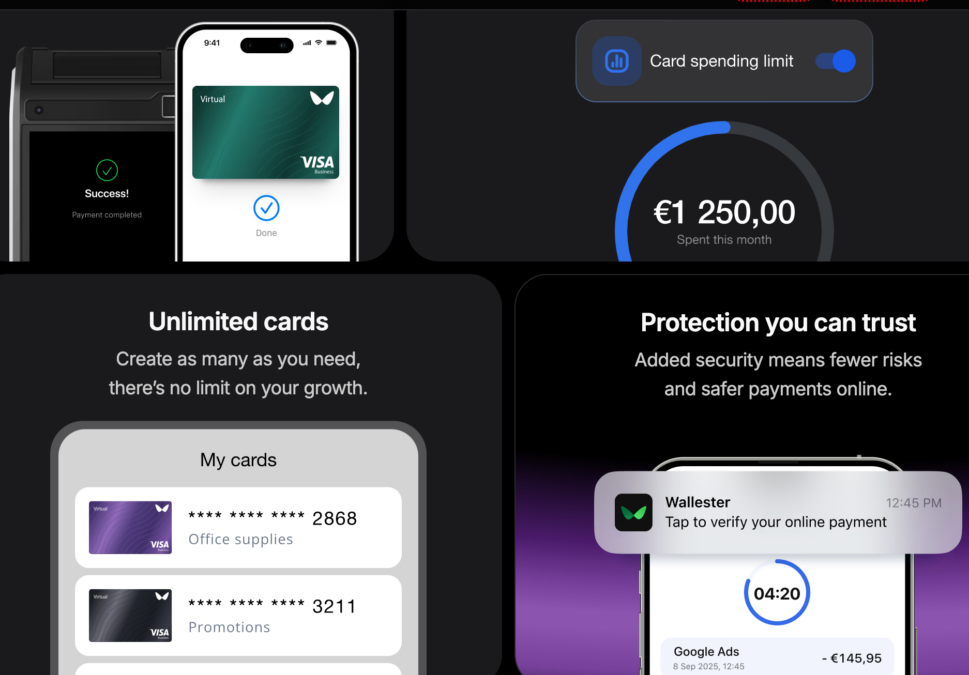

4. Wallester Business: Scalable European Infrastructure

Wallester Business is a Visa principal member issuing corporate cards tied directly to European IBAN accounts.

- Aggressive Free Tier: Offers a “Free” tier that includes the issuance of up to 300 virtual cards per month with zero maintenance charges.

- Limitless Scalability: Additional cards cost minimal fractions of a euro (€0.35 on Free, €0.10 on Platinum).

- Developer API: Integrates card issuance, budget allocation, and real-time transaction tracking directly into your proprietary CRMs.

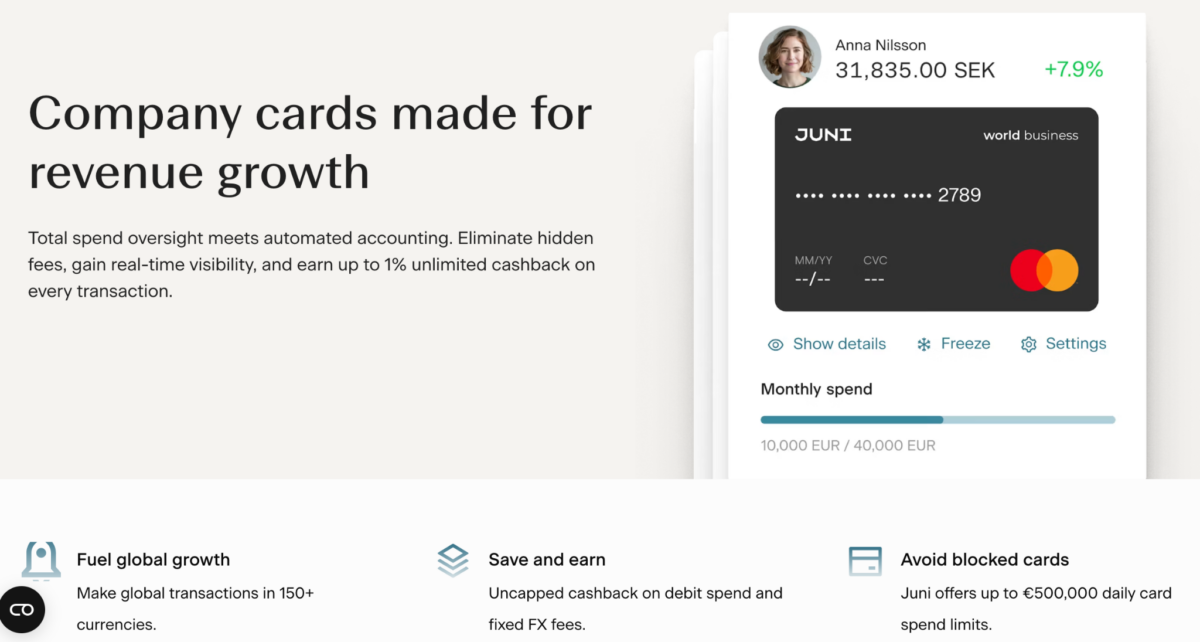

5. Juni: The E-Commerce and Performance Marketing Partner

Juni combines multi-currency business accounts with exceptionally high-limit virtual cards and aggressive cashback incentives.

- Staggering Daily Limits: Up to 500,000 in USD, EUR, and GBP per day, ensuring viral campaigns are never interrupted.

- Unlimited Cashback: Earn up to 1% back on all operational spend to optimize capital efficiency.

- AI Receipt Matching: Automatically fetches and matches digital receipts from ad platforms directly to the point-of-purchase transaction.

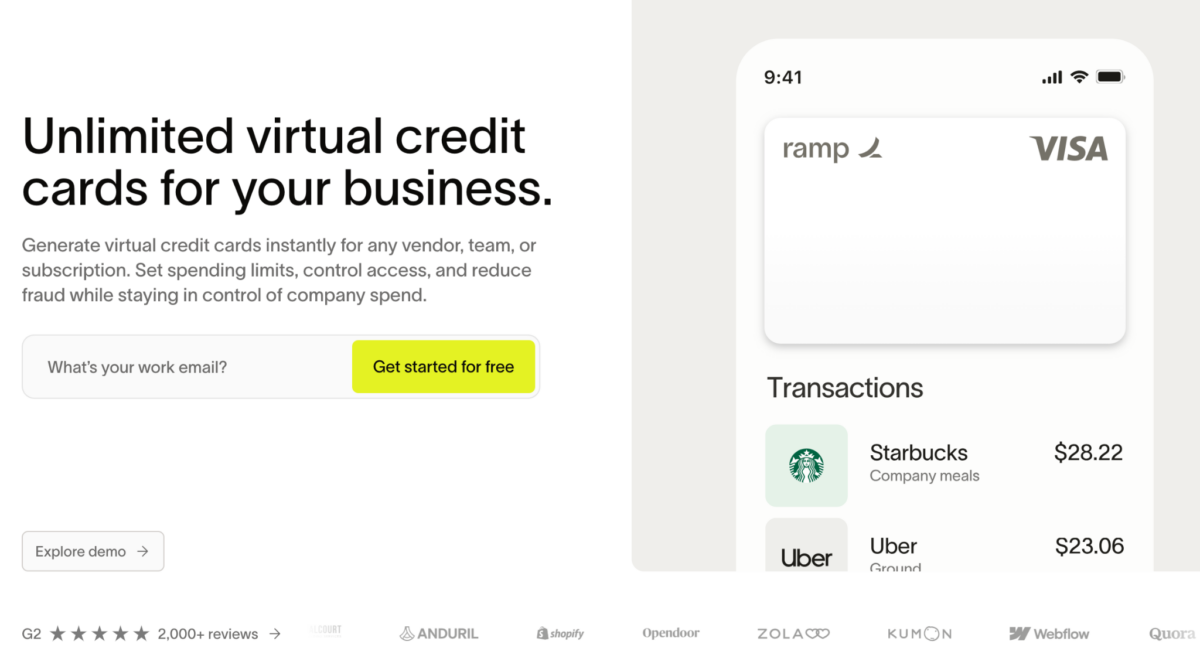

6. Ramp: The Cash Flow and Expense Management Titan

Ramp focuses on comprehensive corporate cost reduction and automated accounting for US-based digital agencies.

- Dynamic Limits: Credit limits scale based on annualized revenue, cash flow, and live bank balances (typically requires a $25,000 minimum balance).

- Absolute Predictability: Zero annual fees, zero card issuance fees, zero foreign transaction fees, and a flat 1.5% cashback on all eligible purchases.

- Pinpoint Restrictions: Instantly lock a card exclusively to a specific merchant category. (Note: Strictly limited to the U.S.-registered entities).

7. Brex: The Venture-Backed Startup and Agency Standard

Brex shares architectural similarities with Ramp but differentiates itself through a highly lucrative, points-based rewards ecosystem.

- No Personal Guarantee: Assesses credit limits based on funding history and cash reserves (often requires $50,000 minimum).

- Aggressive Multipliers: Up to 7x points on rideshares, 4x points on travel, and 2x points on recurring software subscriptions.

- Unique Redemptions: Redeem points for executive coaching, mental healthcare, or Out-of-Home (OOH) advertising campaigns.

8. FuncCards: High-Trust BINs for Global Arbitrage

FuncCards caters explicitly to professional media buyers handling extensive global ad profiles.

- Pre-Tested BINs: Access to premium Credit and Prepaid High-Tier cards that maximize acceptance rates on Meta, Google, and TikTok.

- Proactive Rotation: Continually monitors BIN health in real-time, retiring ranges that show algorithmic fatigue.

- 24/7 Funding: Seamless crypto-to-fiat liquidity using stablecoins like USDT and USDC.

9. Buvei: AI Advertising and Cross-Border Scalability

Buvei targets the unique challenges of high-volume affiliate campaigns on emerging platforms like TikTok Ads, ChatGPT Ads, and Apple Search Ads.

- Geographic Alignment: Diverse array of virtual Visa and Mastercard credit cards designed to match regional billing environments.

- Immediate Liquidity: Supports seamless cryptocurrency top-ups via USDT (TRC20/ERC20).

- Recurring Billing Stability: Essential for maintaining uninterrupted AI advertising campaigns and SaaS subscriptions.

10. Payoneer & WorldFirst: Global Receivables and Ad Spend

For affiliates routing earnings from global marketplaces into ad spend, these platforms dominate the inbound/outbound lifecycle.

- WorldFirst (World Card): Supports spending in over 150 currencies with zero foreign exchange fees when payments are made in a supported core currency (USD, EUR, GBP) with sufficient balance. Perfect for receiving EUR Cuelinks commissions to fund EUR Meta Ads directly.

- Payoneer: Widely used but features complex fees: 1% for ACH receipts, up to 3.99% for credit cards, and a 1% to 4% FX markup on local withdrawals. Virtual Mastercards carry a $29.95 issuance fee and 3.5% cross-currency conversion fees.

Navigating Regional Complexities: The Indian Digital Market

The Indian digital market requires specialized financial infrastructure to navigate the Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA).

Routing Cuelinks payouts into global ad campaigns through traditional platforms like PayPal can result in up to 4.4% platform fees and a hidden 2% to 4% FX markup. Localized corporate cards solve this:

| Indian Corporate Platform | Key Features and Value Proposition | Foreign Exchange and Fee Structure |

| Karbon Business | Unsecured credit up to ₹15 Cr, automated e-FIRA generation, unlimited virtual cards. | 1% flat fee on inward remittances with a 0% FX markup. |

| RazorpayX | Deep integration with Razorpay gateways, automated tax payments, high SaaS limits. | 2.5% FX markup. Registration and annual fees of ₹1499 per card. |

| Happay EPIC Card | Extreme policy compliance, advanced merchant locking, 45-day credit period. | Lowest-in-class FX markup of 1% + GST. Zero joining or annual fees. |

| Volopay | Advanced expense tracking, SaaS management, Xero integration. | Fees from SGD 20/month. 1.6% + GST FX markup. |

| Skydo / Infinity | Focused on export receivables. Instant FIRA generation. | Flat fee models (e.g., $19-$29) or 0.5% flat fee with live mid-market rates. |

The Convergence of Web3 and Virtual Cards

A rapidly expanding segment of the creator economy operates entirely on blockchain architecture. A new generation of cards bridges the gap, allowing direct spending of USDT and USDC without centralized exchange delays:

- MetaMask Card: Powered by Mastercard, allows users to spend tokens directly from their Web3 wallet via networks like Linea and Base. Crypto is converted to local fiat instantly at the point of sale.

- Oobit: Supported by Tether, enables users to connect external wallets and process payments via Apple Pay or Google Pay, offering up to 10% cashback on eligible tokens.

- Fasset: A virtual prepaid model funded with USDT, unlocking immediate global purchasing power over the Visa network.

Beyond Payments: Digital Identity and Networking

While virtual credit cards architect financial operations, “virtual cards” also encompasses Near Field Communication (NFC) digital business cards for in-person networking at industry events:

| Digital Business Card | Core Value Proposition for Creators and Agencies | Evaluation |

| V1CE | Premium benchmark. Focuses on post-tap analytics and lead integration. | 9.8 / 10 |

| Mobilo | Deep CRM tracking to monitor in-person networking conversion rates. | 8.5 / 10 |

| iEdge | Indian market leader. NFC smart cards with embedded CTAs for WhatsApp. | Highly Rated |

| Popl | Optimized for high-volume event networking and booth contact capture. | 7.7 / 10 |

Conclusion: Deploying Your Cuelinks Revenue

The creator economy has matured beyond the capabilities of legacy banking. As you aggregate your earnings through Cuelinks and scale your promotional efforts, relying on a single, static physical credit card introduces catastrophic vulnerabilities.

By funneling your Cuelinks payouts into specialized programmable virtual credit cards, you establish a resilient, scalable foundation.

Platforms like Karat, PST.NET, Spendge, and Wallester provide the automated accounting, deep BIN liquidity, and real-time risk isolation necessary to scale your affiliate empire securely in the 2026 digital economy.

Bonus (on popular demand): Best Virtual Cards for OnlyFans Creators!

For creators and subscribers navigating platforms like OnlyFans, privacy and security are top priorities. Many users prefer to keep their subscription charges off their primary bank statements. Furthermore, OnlyFans requires payment methods to be 3D Secure enabled to process transactions successfully.

Here are the best virtual card options tailored specifically for privacy on this platform:

- Rewarble: This service allows users to purchase an OnlyFans gift card voucher that instantly generates a virtual Visa or Mastercard. The transaction appears as a generic “Rewarble” top-up on bank statements, keeping the activity discreet.

- Privacy.com: This platform provides virtual cards that mask actual payment information to protect against data breaches. Users can set strict spending limits or create single-use cards to manage their subscription budgets effectively.

- Getsby: Offering both disposable and reloadable virtual Mastercards, Getsby is a popular choice for various creator platforms. Using a Getsby card ensures that the platform name does not appear on your personal banking records.

- PlasBit: For those who prefer dealing in cryptocurrency, PlasBit allows you to deposit crypto and load it onto a virtual card. This card can then be added as a payment method on OnlyFans, ensuring the charge remains off regular credit card statements.

- Digital Cash: This is a fully digital prepaid Mastercard that is specifically 3D Secure enabled, making it compliant with OnlyFans’ strict payment security requirements.

Note: While these virtual cards protect your financial data and clean up your bank statements, remember that true anonymity is limited. OnlyFans still requires legitimate payment details behind the scenes for age verification and fraud prevention.

FAQs

How exactly do virtual cards speed up my affiliate payouts?

Traditional payout methods like wire transfers or local bank checks require manual processing times, clearance windows, and intermediate bank checks that can stall your money for days or weeks. Virtual cards bypass the legacy banking delays entirely. This means you get immediate access to your capital without waiting for standard banking clearance

Can I use these virtual cards to directly fund my digital marketing campaigns?

Yes, this is one of the biggest advantages for scaling publishers. This creates a clean, automated loop where your earnings instantly fuel your reinvestment, removing the need to pull from personal bank lines.

Are virtual cards secure enough to handle large commission volumes?

Virtual cards are significantly more secure than traditional physical cards or direct bank links. They leverage tokenization, a security protocol that replaces sensitive payment data with a unique encrypted token during the transaction process. This ensures that the underlying funding account is never exposed to the merchant, effectively neutralizing the risk of mass data breaches.

Sahil Ajmera is content writer with more than 7 years of work experience in field of Affiliate Marketing, Digital Marketing, etc. He loves saving money on everything. His aim is to get readers exactly what they are looking for and that too without wasting much of their time. Whatever he is writing on, you are sure to find a way to earn & save good!